Rolling/Time series forecasting¶

Features that are extracted with tsfresh can be used for many different tasks, such as time series classification, compression or forecasting. This section explains how one can use the features for time series forecasting tasks.

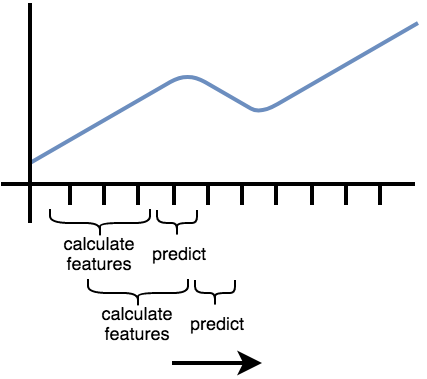

Lets say you have the price of a certain stock, e.g. Apple, for 100 time steps.

Now, you want to build a feature-based model to forecast future prices of the Apple stock.

You could remove the last price value (of today) and extract features from the time series until today to predict the price of today.

But this would only give you a single example to train.

However, you can repeat this process: for every day in your stock price time series, remove the current value, extract features for the time until this value and train to predict the value of the day (which you removed).

You can think of it as shifting a cut-out window over your sorted time series data: on each shift step you extract the data you see through your cut-out window to build a new, smaller time series and extract features only on this one.

Then you continue shifting.

In tsfresh, the process of shifting a cut-out window over your data to create smaller time series cut-outs is called rolling.

Rolling is a way, to turn a single time series into multiple time series, each of them ending one time step later than the one before.

The rolling utilities implemented in tsfresh help you in this process of reshaping (and rolling) your data into a form, so that you can apply the usual tsfresh.extract_features() method.

This means the step of extracting the time series windows and the feature extraction is separate.

Please note that “time” does not necessarily mean clock time here. The “sort” column of a DataFrame in the supported Data Formats gives a sequential state to the individual measurements. In the case of time series this can be the time dimension while in other cases, this can be a location, a frequency. etc.

The following image illustrates the process:

Another example can be found in streaming data, e.g. in Industry 4.0 applications. Here you typically get one new data row at a time and use this to, for example, predict machine failures. To train your model, you could act as if you would stream the data, by feeding your classifier the data after one time step, the data after the first two time steps etc.

In tsfresh, rolling is implemented via the helper function tsfresh.utilities.dataframe_functions.roll_time_series().

Further, we provide the tsfresh.utilities.dataframe_functions.make_forecasting_frame() method as a convenient

wrapper to fast construct the container and target vector for a given sequence.

Let’s walk through an example to see how it works:

The rolling mechanism¶

We look into the following example flat DataFrame in tsfresh format (see Data Formats). Rolling also works for all other time series formats.

| id | time | x | y |

|---|---|---|---|

| 1 | 1 | 1 | 5 |

| 1 | 2 | 2 | 6 |

| 1 | 3 | 3 | 7 |

| 1 | 4 | 4 | 8 |

| 2 | 8 | 10 | 12 |

| 2 | 9 | 11 | 13 |

where you have measured the values from two sensors x and y for two different entities (id 1 and 2) in 4 or 2 time steps (1, 2, 3, 4, 8, 9).

If you want to follow along, here is the python code to generate this data:

import pandas as pd

df = pd.DataFrame({

"id": [1, 1, 1, 1, 2, 2],

"time": [1, 2, 3, 4, 8, 9],

"x": [1, 2, 3, 4, 10, 11],

"y": [5, 6, 7, 8, 12, 13],

})

Now, we can use tsfresh.utilities.dataframe_functions.roll_time_series() to get consecutive sub-time series.

You could think of having a window sliding over your time series data and extracting out every data you can see through this window.

There are three parameters to tune the window:

- max_timeshift defines, how large the window is at maximum. The extracted time series will have at maximum a length of max_timeshift + 1. (they can also be smaller, as time stamps in the beginning have less past values).

- min_timeshift defines the minimal size of each window. Shorter time series (from the beginning) will be omitted.

- Advanced: rolling_direction: if you want to slide in positive (increasing sort) or negative (decreasing sort) direction. You barely need negative direction, so you probably not want to change the default.

The column parameters are the same as in the usual Data Formats.

Let’s see what will happen with our data sample:

from tsfresh.utilities.dataframe_functions import roll_time_series

df_rolled = roll_time_series(df, column_id="id", column_sort="time")

The new data set consists only of values from the old data set, but with new ids.

Also the sort column values (in this case time) is copied.

If you group by id, you will end up with the following parts (or “windows”):

| id | time | x | y |

|---|---|---|---|

| (1,1) | 1 | 1 | 5 |

| id | time | x | y |

|---|---|---|---|

| (1,2) | 1 | 1 | 5 |

| (1,2) | 2 | 2 | 6 |

| id | time | x | y |

|---|---|---|---|

| (1,3) | 1 | 1 | 5 |

| (1,3) | 2 | 2 | 6 |

| (1,3) | 3 | 3 | 7 |

| id | time | x | y |

|---|---|---|---|

| (1,4) | 1 | 1 | 5 |

| (1,4) | 2 | 2 | 6 |

| (1,4) | 3 | 3 | 7 |

| (1,4) | 4 | 4 | 8 |

| id | time | x | y |

|---|---|---|---|

| (2,8) | 8 | 10 | 12 |

| id | time | x | y |

|---|---|---|---|

| (2,9) | 8 | 10 | 12 |

| (2,9) | 9 | 11 | 13 |

For example, you can now run the usual feature extraction on the rolled data:

from tsfresh import extract_features

df_features = extract_features(df_rolled, column_id="id", column_sort="time")

You will end up with features generated for each of the parts above, which you can then use for training your forecasting model.

| variable | x__abs_energy | x__absolute_sum_of_changes | … |

|---|---|---|---|

| id | … | ||

| (1,1) | 1.0 | 0.0 | … |

| (1,2) | 5.0 | 1.0 | … |

| (1,3) | 14.0 | 2.0 | … |

| (1,4) | 30.0 | 3.0 | … |

| (2,8) | 100.0 | 0.0 | … |

| (2,9) | 221.0 | 1.0 | … |

The features for e.g. for the id (1,3) are extracted using the data of id=1 up to and including t=3 (so t=1, t=2 and t=3).

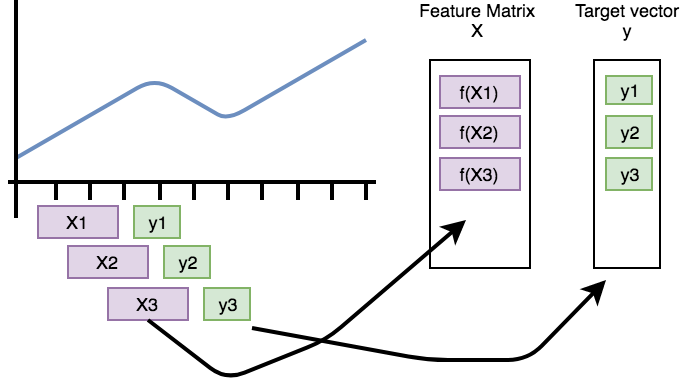

If you want to train for a forecasting, tsfresh also offers the function tsfresh.utilities.dataframe_functions.make_forecasting_frame(), which will help you match the target vector properly.

This process is visualized by the following figure.

It shows how the purple, rolled sub-timeseries are used as base for the construction of the feature matrix X

(if f is the extract_features function).

The green data points need to be predicted by the model and are used as rows in the target vector y.

Be aware that this only works for a one-dimensional time series of a single id and kind.

Parameters and Implementation Notes¶

The above example demonstrates the overall rolling mechanism, which creates new time series. Now we discuss the naming convention for such new time series.

For identifying every subsequence, tsfresh uses the time stamp of the point that will be predicted together with the old identifier as “id”. For positive rolling, this timeshift is the last time stamp in the subsequence. For negative rolling, it is the first one, for example the above dataframe rolled in negative direction gives us:

| id | time | x | y |

|---|---|---|---|

| (1,1) | 1 | 1 | 5 |

| (1,1) | 2 | 2 | 6 |

| (1,1) | 3 | 3 | 7 |

| (1,1) | 4 | 4 | 8 |

| (1,2) | 2 | 2 | 6 |

| (1,2) | 3 | 3 | 7 |

| (1,2) | 4 | 4 | 8 |

| (1,3) | 3 | 3 | 7 |

| (1,3) | 4 | 4 | 8 |

| (1,4) | 4 | 4 | 8 |

| (2,8) | 8 | 10 | 12 |

| (2,8) | 9 | 11 | 13 |

| (2,9) | 9 | 11 | 13 |

which you could use to predict the current value using the future time series values (if that makes sense in your case).

Choosing a non-default max_timeshift or min_timeshift would make the extracted sub-time-series smaller or even remove them completely (e.g. with min_timeshift = 1 the (1,1) (i.e. id=1,timeshift=1) of the positive rolling case would disappear).